Shot Tower Capital has now completed its report to the board of the Hipgnosis Songs Fund, or SONG, the London Stock Exchange-listed music rights investment fund. The results were published just before the Easter Weekend.

Its assessment of how investment advisor Hipgnosis Song Management has run operations for SONG is blistering, and contains a wide range of astonishing allegations, including poor systems, missing documents, misleading statements, excessive spending and legal ineptitude.

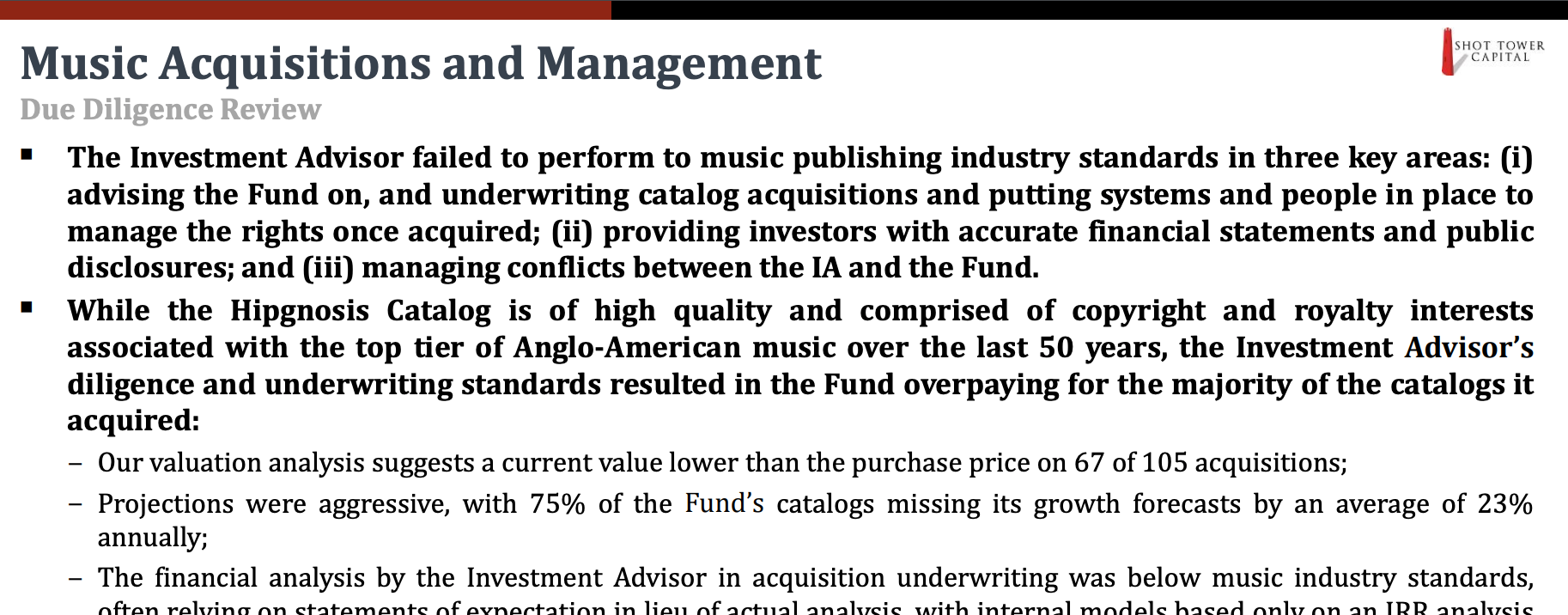

Most damning is STC’s accusation that HSM’s “diligence and underwriting standards” means that SONG overpaid for “the majority of catalogues it acquired”. In fact, says STC, 67 out of the 105 catalogues acquired have a valuation that, by its analysis, is lower than the price SONG paid.

This is the latest chapter in the continuing Hipgnosis saga, and is part of the ongoing strategic review of SONG, which was instigated by the old board shortly before they were ousted and replaced by a new board.

The strategic review has been characterised by some as a falling out between SONG - now chaired by Robert Naylor, previously chair of the Round Hill Music Fund - and Hipgnosis Song Management, run by Merck Mercuriadis, who founded both SONG and the other Hipgnosis companies.

As the review has progressed, there has been a series of acerbic announcements by both sides, with a flurry of briefing and counter briefings - and, recently, some significant adjustments to key financials that underpin the fund. The most recent of those saw two rapid, significant downward adjustments to the NAV or Net Asset Value of SONG, and a corresponding drop in share price.

The strategic review is due to wrap up fully by 26 Apr, but meanwhile SONG has summarised the contents of the due diligence report prepared by STC, and published them for investors to review. The results are, by any reading, fairly startling.

A measure of quite how startling comes in the shape of a press release issued by HSM shortly after SONG announced that the report was available for investors, in which it said “there are aspects of the report that HSM strongly disagrees with and considers to be factually inaccurate and misleading”.

So what are the key allegations made by STC - and what do they mean? CMU has gone through the report in detail and picked out the most significant.

Some news is good. The total catalogue of songs held by SONG “represents a high-quality mix of catalogues containing copyright and income streams derived from compositions performed by some of the top artists of the last 50 years”, STC says.

Streaming is the fastest growing royalty stream making up 32.5% of the fund’s revenues in the last twelve months, versus 28.7% in 2021. As “more contemporary” catalogues acquired by the fund mature their incomes are beginning to stablise, after “significant revenue declines in younger catalogues following purchase”.

At one level this is not a huge surprise - new music has a limited window during which it has its highest velocity potential to generate revenue - and with it a limited window where it still feels new and fresh, before it begins to feel like yesterday’s trend.

When songs are new they are being toured, being synced and being streamed more heavily - but two or three years in that window of attention has dropped off; touring may involve new songs and sync buyers may not want to use a three year old song if they can use something fresher.

Another interesting point made by STC is that the SONG catalogue generates “limited revenue from non-English language markets”, pointing out that those markets represent the highest growth streaming markets.

Also surprisingly, STC says that SONG’s passive catalogues “grew significantly better” than catalogues being actively managed by HSM.

Alongside this is the allegation that HSM “failed to invest in systems and provide the services required” to effectively manage the catalogues, and that HSM, “six years since the inception of the fund, is still not tracking or managing the Hipgnosis Catalogue at the song level”, which, STC says, is “standard for the music publishing industry”.

“Key documents” are also missing from acquisition files, STC adds, and it’s unclear whether those documents were not obtained or are “just unable to be located”.

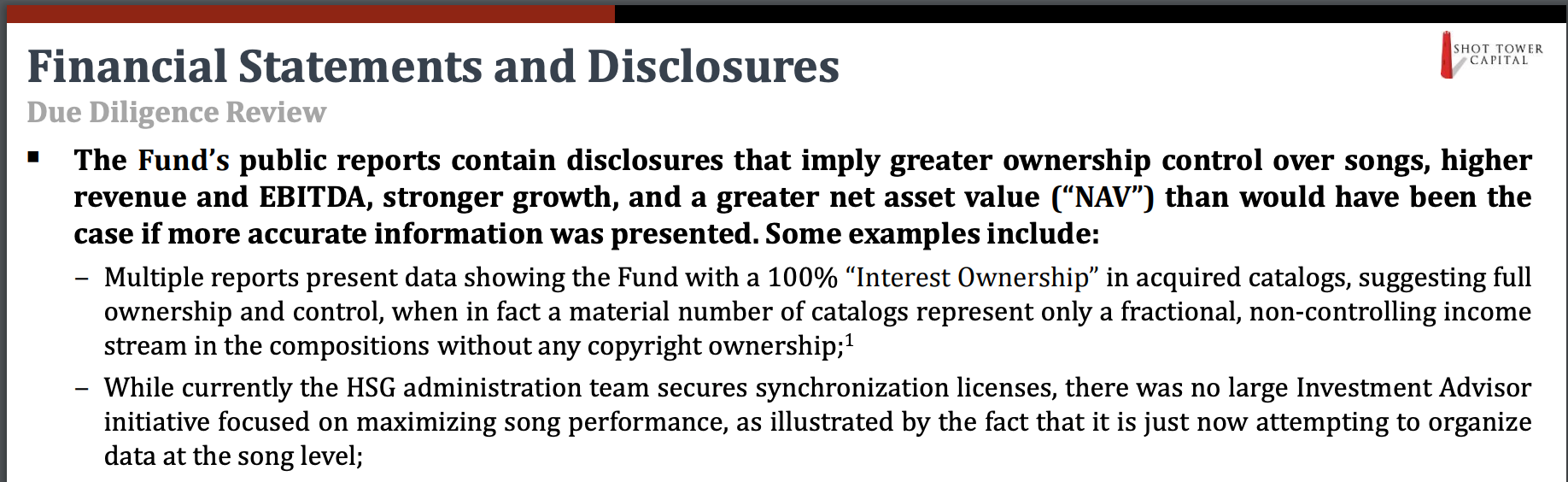

Valuation and revenue streams aside, it’s the conduct of HSM that Shot Tower really goes to town on, alleging significant irregularities in how key financial metrics were presented and communicated to investors. More remarkable are allegations that “data in the financial systems” was “completely different” to information presented in public disclosures.

Additionally, SONG’s public disclosures to investors contain statements “that imply greater ownership control over songs” with “multiple reports” showing a “100% ‘Interest Ownership’ in acquired catalogues suggesting full ownership and control”, when in reality a “material number” of catalogues were non-controlling income streams, with no copyright ownership.

Between $1.5 million and $2 million was spent annually by SONG for “award shows and public relations, including significant payments to music industry periodicals” and there are “multiple areas” where expenses appear “unrelated to the Fund” or “excessive”.

One of the most significant allegations relates to a previous claim made of “double counting”. The STC report provides more detail on this, saying “it’s common in music catalogue acquisitions to have an effective date that aligns with the start of a royalty accounting period to simplify the hand-off of royalty accounting from a seller to a buyer when a closing date occurs mid-cycle. Any cash received by the seller after the effective date and prior to closing is credit to the buyer via a purchase price adjustment at closing”.

In simple terms this means that the contract might have two dates - the “effective date” at which point the catalogue is deemed to have changed hands, which might be earlier than the “closing date” at which point all documentation and transfers should take place. If royalties continue to come in to the seller during that window, then this is subtracted from the purchase price at the closing date. So if a deal was done for $2 million with an effective date of 1 Oct and a closing date of 31 Jan, and $200,000 of royalties were paid to the seller between those two dates, then the actual purchase price reflected in the fund's financials would be $1.8m.

What STC is alleging HSM started doing is to “negotiate effective dates that were multiple royalty periods prior to closing” and, rather than making a “price adjustment on the balance sheet”, would report the “pre-closing income as fund income on the closing date”.

This means that - to take the example above - on 31 Jan the acquisition price would be reflected as the full $2 million, with $200,000 being reported as revenue on the same date, without a corresponding deduction being made against the acquisition price.

In addition, says STC, there were “specific negotiations” where a deal on price and date was agreed but HSM then “negotiated an earlier effective date and an increase in purchase price on a dollar-for-dollar basis for ‘revenue purposes’”.

Overall, the damning report from STC seems to contribute to the overarching narrative hinted at by SONG in recent announcements that it may take legal action against HSM for breach of contract.

If this happened, HSM’s “call option” - that gives it the right to bid for SONG’s catalogues and which has been a point of contention in recent months - would cease to have effect, potentially clearing the way for a sale of the SONG portfolio.

Speaking to Citywire, longtime HMS naysayer, Stifel’s Sachin Saggar, said that the report looks “very bad” for HSM and that it would be “difficult for the board to justify anything other than a termination for cause”.

SONG’s share price jumped 8% after the report was released, interpreted by some analysts as a sign that investors now see the most likely option is that either the fund is wound down with the catalogues being sold off or that one buyer may step in to acquire the entire operation. With further announcements expected from both sides in coming weeks, there’s sure to be more drama to come.